Managing A Treasury For Sustainable Growth

Whether it is a team or a DAO, to survive longer term in crypto these entities need a reserve of funds to pay for maintenance, development, incent growth of their project, and have ‘rainy day funds’ for emergencies or opportunities. This so-called treasury should provide this funding, especially during crypto’s predictable bear markets. Growing projects often have to tap into these reserves since they may not generate ample revenue yet, or previously sufficient revenue is not generated during poor market conditions. In bear markets teams often become inactive or rug, because they lack the funds to continue development. How can a project ensure their long term viability, manage risk, and steadily grow their treasury? For investors and traders these questions matter too since they can point to stronger and weaker projects in the market.

In this article we discuss several considerations for project teams which we consider essential choices in building a healthy treasury. On top of that we give pointers that help ensure long term project survival. We understand that a lot of projects might be facing bad weather already considering the market conditions, but hopefully our work reaches projects or future projects to prevent them from making these mistakes. As always, this is not financial advice, but a thought piece to stir up conversation regarding treasury management.

An example of a proposal to change allocations in the protocol controlled value (PCV) to stable coins after heavy losses on these holdings. Even though the treasury is often a smaller part of the PCV, this example shows value managed by protocols gets hurt in bear markets.

The current state

According to the Messari “Crypto Thesis for 2022” based on DeepDAO data the biggest allocation, by far, in top DeFi treasuries is the native token. This is logical since these projects generated the tokens and have various mechanisms in place to distribute the tokens to incentivize the community. Not only the bigger projects in DeFi and crypto at large, but also smaller ones often have a large exposure to their own tokens.

However, a big allocation to the native token introduces the problem that the project is directionally exposed to their own asset, which means it is at the mercy of price fluctuations in fiat. Even if you think crypto will replace fiat, the fiat value can still matter for people being incentivized by the project and determines your real world purchasing power, including costs like administration, legal, compliance, offices and so forth. The problem is that by holding too many of their own tokens in the treasury, projects double down on their own success. This often results in teams not having enough funds available to continue when they are needed most, during unfavorable market conditions with little incoming revenue. They have to deliver their product, but also need to maintain the value of their token. The latter is often out of their control since the valuation of the token is a result of the opinions and actions of the market participants.

In addition to their own native token, these projects hold additional crypto market risk since they might have accumulated assets like ETH, SOL, AVAX, or FTM in their pre-sales, or because they accumulated these assets by buying them on the market or generating them as revenue.

In our opinion, projects should reduce this directional market risk on their own token and other crypto assets for longer term survivability. A shift to more sustainable allocations or a hedge strategy protects projects from depreciating USD value of their treasuries.

General guidelines

The main function of the treasury is to sustain maintenance and development of the project as long as possible. Stability and predictability should be front and center when making decisions on the allocations.

Trading with the funds is a stark contrast to focusing on predictability. The most iconic example of a project trading with their own funds happened in 2018, when Substratum admitted they were trading their own treasury, while eventually they burned through $13 Million in assets and eventually had to lay off their staff after 2 years. The moment supreme was Substratum admitting they were shorting Ethereum at almost the exact bottom of the bear market. This example should remind projects to stay to their craft and focus on shipping their product instead of trying to run a trading floor. A situation when trading makes sense is when the position is a hedge against the holdings in their treasury, i.e. shorting their own native token to be delta neutral and lock in USD value or a basis spread.

Protocols might have coins in their treasury they need for development or to operate business. Examples could be: ETH (or any other ecosystem coin) to pay for transactions or purchase governance tokens of partner protocols. While these can be considered holdings, they are actually business costs and allocations should remain modest. Projects might be better off not counting these funds in the total of treasury funds and offset them as costs paid for by protocol revenue or investor funds.

Projects must also be mindful of downside reflexivity. Treasury allocations should be made to withstand the worst market conditions, however since most projects are founded in bull cycles and their tails, it can result in overly optimistic models. They would be wise to make key expense commitments in fiat denominations and to count on these being paid with stablecoins. Pre-revenue and Product Market Fit projects would be wise to balance and keep at least 2 years of runway in stablecoins.

Stablecoins

But steady-state and extreme-case soundness should always be one of the first things that we check for.

Vitalik on stablecoins. Source: https://vitalik.eth.limo/general/2022/05/25/stable.html

Stablecoins (also referred to as stables) are the essential part for (as the name suggests) bringing stability to a treasury. Stablecoins are a hedge against the crypto volatility, which already is affecting projects since the inflow of funds and users often is correlated with the up and downward movements in coin prices. When choosing which stablecoins to deploy in the treasury understand what backs the stablecoins and go for the most battle tested long standing coins. The Lindy Effect is a great rule of thumb to help with decision making. Projects should avoid experimental (often algo-stablecoins) and younger stablecoins since they have a higher chance of losing their peg. A recent example of problems with an experimental backing mechanism on a fairly young project was UST losing the peg when LUNA lost value in USD.

Below are some suggestions of which stablecoins we assume to hold their peg for a longer foreseeable future. All of these attempt to maintain a value of 1.00 USD.

USDC is a stablecoin brought in circulation by Circle and is fully backed by the US dollar or US dollar denominated assets. Every month a report is issued in which Accounting firm Grant Thornton LLP provides proof of the backing. These reports go all the way back to October 2018. USDC is used by many centralized exchanges like Binance, Coinbase and Kraken, and can be used across many different blockchains like Ethereum, Avalanche, Solana etc.

USDT issued by Tether is the stablecoin with the highest market cap and even ranks 3rd on the total market cap ranking. Active since 2014, this stablecoin surely passes the Lindy test. USDT is backed by various assets which are mentioned in their independent accountant report. The assets are: cash, cash equivalents (money market funds, U.S. Treasury bills), commercial paper and certificates of deposit, corporate bonds, secured loans and other investments including digital currencies. In the past the backing was sometimes controversial since Tether only started publishing reports on the backing of USDT early in 2021 and there is question of how quickly Tether can convert the non-cash holding to cash if stablecoin holders want to redeem their USDT. However, even if the peg was slightly lost during moments of high market volatility in the past, the redemption mechanism made sure to restore peg quickly and thus ensured stability. Similar to USDC this stablecoin can be used across the most used exchanges and blockchains.

The backing of Tether. Source: https://tether.to/en/transparency/#reports

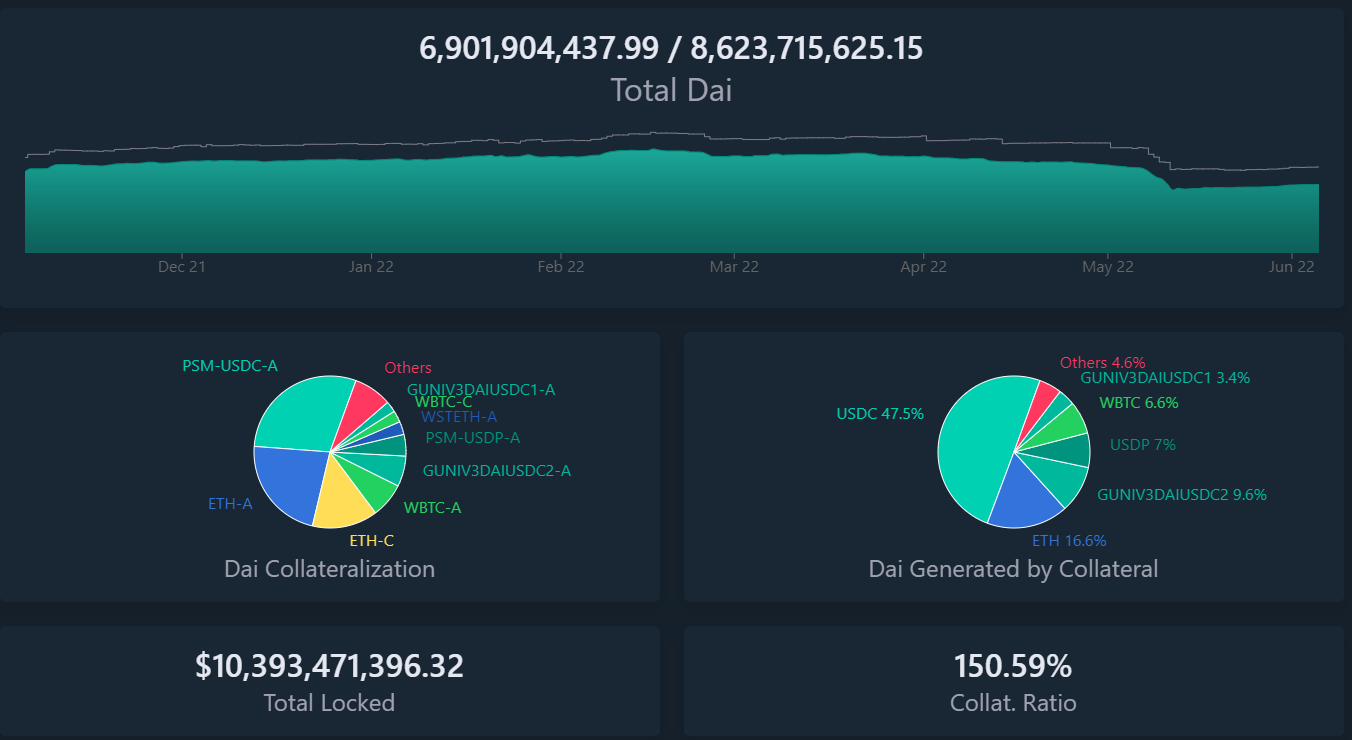

DAI takes another route by being a decentralized stablecoin, which is backed by the collateral on the Maker Protocol and is supported on Ethereum and other blockchains. Maker Protocol is governed by MKR holders who decide on which assets can be collateral and which risk parameters to apply to the protocol. DAI is used across plenty of the most used blockchains. For a great overview on which chains, protocols of platforms DAI is being used see this Dune Dashboard.

The backing assets for DAI. Source: https://daistats.com/#/

Several public independent articles and tools can be found to help forming a better judgement on stablecoins. Curve Risk Assessment reports are great for underwriting of stablecoins. They help determine what justifies being whitelisted on the Curve Gauge. Another useful tool is stablecoins.wtf, where you can see interesting metrics such as the velocity of stablecoins (market cap / volume), historical peg and market caps.

Non-stable coins

In this paragraph we discuss the holdings in the native token, but also the holdings in for example BTC, ETH or the ecosystem coins like AVAX, SOL or FTM. These coins are the assets that are exposed to directional market risk since they can fluctuate in USD. In bullish market conditions these coins can be great to have in a treasury, but in bearish market conditions these lose value fast, which makes funding development harder if you depend on them for your funding needs. The allocations to these coins can vary based on market conditions. Maybe counter-intuitively, the longer a bull market continues, the lower the allocation to these tokens should be. For example the Ethereum foundation timed their selling quite well since they sold the tops in 2018 and in 2021. In contrast to bullish conditions, in bear markets these coins can be accumulated since the potential to increase in value is higher. For projects it might be better to seek counsel from a more experienced position or swing trader to assist with finding the moments to accumulate for the long term and moments to slowly start selling.

The native token for the project is almost always part of the treasury if a token is issued. The native token needs to be held in the treasury often to incentivize the community, to pay for development and is needed for project functioning. Selling of the token on the market can lead to accusations of dumping or rug pulling, but in some moments selling is needed to fund development of the project further. Projects might want to consider OTC sales with approval of the team, community or other voting entities that are required within the governance framework. Another option, if futures are available, is to short their own token to lock in the dollar value of the tokens. The price for maintaining this position is the funding or premium on the future, but reduces the directional exposure. In some cases the project wants to buy back their own token through treasury funds if they are confident in their own ability to deliver the product, or the token is bought back with fees generated by the product. These strategies work best during periods of a sideways market or after a sustained bear market.

Building in crypto is a bet on the space or on specific ecosystems, which can be represented in treasury allocations. Projects may decide to hold BTC or ETH as these can be considered the most reliable assets and assumed to appreciate in value over longer periods of time. The percentage allocation can vary in bull and bear markets to optimize the USD value and reduce risk. The project might also want to have exposure to the token of the ecosystem they are building in, which in general is more risky. Popularity and usage of ecosystems in crypto fluctuate and projects may and often are building across multiple chains to reduce this risk. The same should apply to treasury allocations, where weightings of ecosystem tokens need to be small because of their risk.

Maybe redundant to note but these assets add directional long exposure. The position should be in spot and not in futures. As stated earlier in this article, trading with the treasury, particularly with leverage, shouldn’t be done by team members or developers, if at all.

Passive income strategies

DeFi brings plenty of opportunities to allocate idle funds and generate passive income. The passive income can function as a means to grow the treasury or fund the project, while also contributing to the liquidity in DeFi. Whether it is with stable coins, ETH or ecosystem coins these options might be giving a good APY.

Vaults like those deployed by Yearn, Convex or Robovault. These are staking pools that generate returns. Most are delta-neutral and provide returns for deposit tokens without incurring directional exposure. The benefit is that these protocols automatically shift capital to find the best farming opportunities, which reduces the time and fees to manage the capital manually. Returns are often highly correlated to market prices, since most yield comes from token rewards (e.g. emissions) rather than trading fees (say 0.04% trading fee on Curve).

Collateralized money markets like Aave and Compound can be utilized to store assets and earn interest when others borrow assets. Although the APY can vary over time because of utilization of these markets, the APY in most cases can still give a good APY over a longer period.

Undercollateralized lending markets like Maple, TrueFi and Goldfinch. Compared to other money markets these APYs are higher since these are undercollateralized and require less collateral or no collateral to borrow with, but capital is lent to real world businesses. Maple’s and Goldfinch’s borrowers both sign lending agreements that permit real-world recourse and have differing degrees of off-chain collateralization via real-world assets. Maple borrowers are vetted by leading credit experts, while Goldfinch borrowers will be vetted by Auditors, who are community members that have staked the GFI token. Importantly, interest payments are often in stablecoins, making yields more dependable in weak markets.

Delta neutral strategies can be deployed by the protocol themselves or third parties. In some market conditions shorting the tokens in the treasury on futures with spot as collateral can generate income from funding or the premium on quarterly futures, while reducing the directional risk. Market makers like Alameda and Amber Group offer services to help clients earn passive income in floating and fixed rate products to relieve you of the handling of these positions.

Liquidity Provision is a smart way for treasury funds to earn fees. This is done by providing the native asset, or other crypto assets, and stablecoins to a decentralized exchange (DEX) like Uniswap or Sushiswap. This idea of protocol owned liquidity (POL) was popularized by OlympusDAO, allows the team to generate trading fees, and always have some exposure to stablecoins and their treasury assets depending on market conditions. Services like Arrakis (by Gelato Network) automate Uniswap V3 range rebalancing and can be attractive passive solutions.

All of these above options have different risk profiles, since there can be smart contract risks, collateral risk and third-party risk. Spreading between various options helps for minimizing the total risk of allocated funds.

Conclusion

A treasury should consist of assets that provide stability but maintain development and community incentivization. This treasury is a safety net for difficult times, while the team can prepare for better market conditions that often bring more volume and thus more revenue. Allocations in the treasury can consist of a mix of stables and non-stable assets to capture the upward movements of the crypto market, but can be changed over time to protect for downside. Maintaining a treasury requires continuous effort and should be a regular discussion point in the team or in the DAO. If your team needs help, feel free to reach out to us Deus Ex DAO, an investment syndicate and community of crypto-native experts who can be a sparring partner and advisory partner for your project.