Power Tokens #1: A new Tokenomics Template

From ve-tokens to pw-tokens?

It is not often that we witness the release of a new tokenomics model in crypto. Therefore, IPOR sparked our (and others’) attention when they published their article on power tokens.

In DeFi, three major tokenomics standards have existed so far:

Simple staking model: A user stakes tokens and can withdraw anytime. Tokens are translated 1-to-1 into staked tokens.

Vote escrowed (“ve”) tokens: Invented by Curve Finance. A user locks tokens for a selected amount of time. The tokens cannot be withdrawn before the chosen staking period ends. The conversion rate from tokens to staked ve-tokens is dependent on the lock-up period a user chooses: The longer the lock-up period, the more ve-tokens they receive. Here, The assumption is that the longer a user locks up their tokens, the more aligned they are with the protocol, and the more weight they should have in governance and revenue sharing. The ve(3,3) model popularized by Andre Cronje with Solidly intended to improve on this, by adding 1) tradable veNFTs as a representation of a user’s staked balance to counteract centralizing forces by protocols like Convex, 2) non-dilution of stakers, and 3) stakers only receiving rewards from pools they voted for with the goal of aligning governance and economic incentives.

Time-based multipliers: A user stakes tokens and can withdraw anytime. Tokens are translated 1-to-1 into staked tokens. A user linearly accrues multiplier points over time which makes them eligible for a larger share of rewards. The maximum multiplier is usually capped to prevent early entrants from dominating new stakers, which would make the token unattractive for non-holders to buy into.

Teams also experimented with additional properties like reward vesting, withdrawal delays, (early) withdrawal fees, etc.

The vote escrowed token model has been the most copied token design in the last two years. Teams saw its success, copied the idea for their own projects and received positive feedback from the market (who saw it work for Curve, and thought it would too for the project at hand). So it worked! Or did it?

The goal of ve-token design is to better align incentives between the protocol and its token holders. Over time, its own problems came to light, as we covered before.

The questions now become: Can power tokens solve the issues of ve-tokens? And what challenges do we have to look out for?

What is a Tokenomics Template?

Before diving deeper into the actual tokenomics, let’s take a look at why we call power tokens a potential tokenomics template in this article’s title.

A template must allow others to easily use and adapt it to their own needs.

Curve’s ve-token design made it difficult for teams to fork as it was closely intertwined with the Curve protocol and its massive adoption, which allows offsetting its large emissions.

IPOR takes a modular approach to its token system design, abstracting the logic of power tokens from the rest. This enables other teams to copy and adjust the open-source code of power tokens to make it fit with their project and token. In the ve-token model, one key hurdle is that a user’s ve-token balance is decided by the conversion logic (where longer lock-up leads to more ve-tokens), with this ve-token balance then being used for governance, liquidity incentives etc.

In the power token model, each token staked translates to one power token. Then, each module built on top, for example liquidity incentives, can interpret power tokens with their own logic. IPOR employs a logarithmic curve for liquidity mining, meaning marginal benefits (token rewards) diminish with an increasing ratio of power tokens to liquidity provided. This is done to incentivize broad distribution of the power tokens and avoid early and large LPs to be able to hog all the boosting benefits. To make it flexible for other builders, this curve can be changed, without requiring any revisions of the staking mechanic.

The need for a new Token Design

A token is a complex puzzle piece to add to a protocol ecosystem and can take on several functions, from bootstrapping a network, incentivizing key activities from participants, making a system more resilient by decentralizing ownership, or creating a community that provides marketing, business development, even software development.

It is impossible for a token to fulfill all potential goals. Some objectives are contradictory in nature. For example, while a token can help fundraise more easily because of its liquidity compared to equity, a large investor allocation is usually detrimental to creating an incentivised community and decentralizing governance. A token can only be optimized towards a limited set of key variables. Therefore, we advise teams to first get a clear view of their business goals, then test product-market fit with an MVP and a couple of iterations, and only afterward release a token to support the product and achieve the overall business goals. The goals of token design follow from the business goals. For instance, a product intended to benefit from (defensible) network effects should have a tokenomic design that incentivizes kickstarting such network effects.

To learn more about our tokenomics philosophy, check out our tokenomics series. Our first article covers how to decide whether a project needs a token.

Good teams manage their token and its design responsibly. The opportunity lies in what the token can achieve for the project, not in the token itself. The value has to outweigh the costs of added complexity of processes (e.g. governance), management of the additional layer on top of the product (e.g. token allocation, liquidity, token value accrual), and noise as a result of having 24/7 evaluation and sentiment management based on the token price.

Over time, the market surfaced several challenges of existing token designs.

Failure to create aligned, active governance participants

The assumption behind ve-tokens that governance participants which lock up their tokens for multiple years are incentivized to vote in favor of the long-term health of the protocol has proven itself to be false.

Reality pain(t)s the following picture: While governance participation may be higher, it’s mostly because of short-term financial incentives (bribes) rather than actual alignment. The issue occurring here is that bribes do not overlap with revenue to the protocol, only to token holders. For example, governance participants direct token incentives to the liquidity pools with the highest bribes. These pools tend to have low trading volumes (otherwise they wouldn’t need such extensive bribes as LPs would earn more fees) and as a result, low fees for the protocol. This is what Solidly attempted to resolve by only allowing voters to share in fees from the pools they’d voted for.

Protocols not only see low revenue from governance decisions. They also vastly overpay in token incentives for the little they make. While bribers can boast “every dollar in bribes unlocks $3 in token incentives for us”, let’s look at this statement from the side of the emitting protocol and its token holders. Token holders get diluted 3$ for every dollar in bribes they make. The protocol makes a couple of cents in revenue for incentivized low-volume trading pairs.

Bribing allows token holders to make short-term profit. “Who knows what the tokens will be worth in 4 years. Better to take with me as much as I can now“. Long-term governance becomes an externality that others are supposed to take care of. Over time, more and more voters see they get the short end of the stick by voting with a long-term vision instead of taking bribes like the rest. With a decreasing price because of others dumping their liquidity mining incentives, the long-term vision fades into the background and bribes become the main utility for the locked tokens.

Boom-and-bust cycles intensifying

ve-locking takes tokens out of circulation for long periods. The remaining liquidity is insufficient to serve the market, especially as ve-token systems usually involve high token emissions.

In the beginning, locking quickly takes tokens out of circulation while attention attracts buyers, driving prices up. Then token emissions start, leading to selling pressure from emission recipients. While stakers can’t dump their principal because it’s locked, new buyers might also not be willing to step in as they are not comfortable locking up their tokens for years (which comes with huge opportunity costs) and otherwise would only get diluted over time. The DeFi whale playbook has been to be an early investor or liquidity provider, to capture the majority of early liquidity mining rewards, potentially locking, but definitely selling a lot of the yield on new entrants.

The people who get rekt in the end are stakers which lock their tokens for the maximum period of time, the voters the protocol actually wants.

Destructive meta-layers (like CVX, Hidden Hand)

For stakers, it makes sense to go through the meta governance protocol as it gives them short-term liquidity for their vote-escrowed position, like cvxCRV for CRV (we’ll use this as an example for simplification purposes, but it’s similar for all). The meta governance protocol accumulates ve-tokens which are controlled by their own native-token (e.g. vlCVX). If owning 1 vlCVX (or bribing vlCVX holders) becomes more effective for DAOs than owning/bribing CRV holders, token demand and bribes are flowing to it rather than CRV.

Another issue of meta governance protocols is the liquidity of the tradable token representing the vote-escrowed, original token, like cvxCRV. To be fair, liquidity is better than zero, as it’s the case with locked tokens during their lockup period. However, while ve-tokens unlock at some point, their wrapped counterpart never will. It’s a one way street from CRV to cvxCRV. The only way to leave is through the cvxCRV/CRV liquidity pool.

Everyone is locking their token through the meta-governance protocol as it’s the game-theoretically optimal solution. Part of the cvxCRV holders want to leave at some point. Now, the only way is to go through the cvxCRV/CRV liquidity pool. The more holders cash out, the more imbalanced towards cvxCRV the pool becomes. Meaning the later you sell, the less CRV you get for your cxvCRV. As a consequence, since you are looking to cash out, you get less USDC/ETH in the end.

The only way for sellers to get a better price again at some point is if others buy cvxCRV “at a discount” to CRV. The problem here is there is no discount. cvxCRV is not pegged to CRV and there’s no redemption mechanism. There’s no additional arbitrage mechanism.

Essentially, by staking with the meta-governance protocols, people trade long-term liquidity (by having to go through the CRV/cvxCRV pool) for short-term liquidity (by receiving cvxCRV for their locked CRV). Projects like Convex and Hidden Hand are logical evolutions to increase the utility and “wars” for ownership of projects that employ ve-Token designs. However they have substantial downsides, and we must demand better as users. They are bolt-ons to solve an innovative but flawed tokenomic design.

For more information about the downsides of ve-tokens, check out these articles:

Power Token Overview

The Power token design has the following goals

Alignment of LPs and stakers

Price discovery without locking stakers

Broad distribution of tokens to increase decentralization

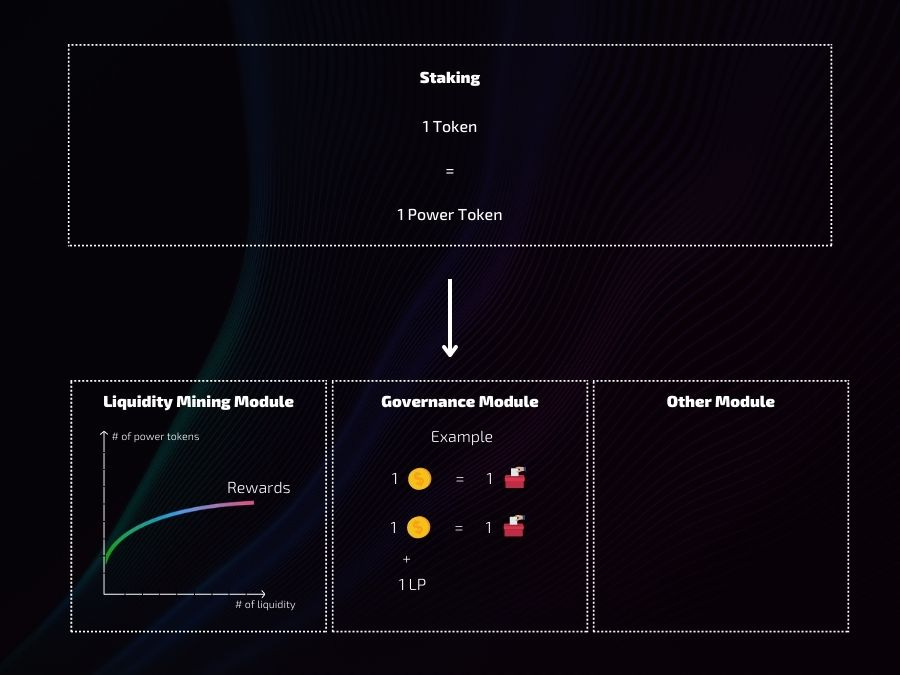

Holders can stake the native-token to receive power tokens 1-to-1. There is no lock-up (!!) but protocols may add a withdrawal period. For IPOR, the first protocol using power tokens, there’s a 14 days withdrawal period.

Compared to the ve-token model where the amount of ve-tokens a user receives is based on their lockup period, there’s no logic embedded into the staking contract. This makes power tokens more flexible as each additional module can have custom logic.

For example, IPOR uses a liquidity mining module with a logarithmic multiplier curve. Therefore, stakers have diminishing marginal returns on power tokens when keeping the liquidity provided constant. The more tokens someone stakes without increasing liquidity (so the higher the ratio of power tokens/LP tokens), the less additional rewards they earn. The reward multiplier still increases, but in a slower manner.

Stakers further have to decide which pools to apply their boost to. Depending on the liquidity provided to a particular asset pool and the staker’s ratio as an LP in it, their potential part of the delegated power tokens, as well as the amount of liquidity mining rewards per pool, a power token staker should seek a game theoretical optimum across asset pools..

Other modules can flexibly be built on top of power tokens, such as a governance module or a profit sharing module.

That’s it for today! In Part 2, we will dive deeper into the mechanics of Power Tokens.